The transportation industry has changed so much in the past few years. Instead of conventional taxis, now users are starting to use freelance transportation services. The benefits of working for one of these companies are seemingly limitless, from creating your own work schedule to meeting new clients on a daily basis.

The transportation industry has changed so much in the past few years. Instead of conventional taxis, now users are starting to use freelance transportation services. The benefits of working for one of these companies are seemingly limitless, from creating your own work schedule to meeting new clients on a daily basis.

But what happens if you’re involved in a wreck while working in this rapidly growing industry? That’s where insurance comes in handy. There are several options to choose from, and some apply in certain situations while others do not. In order to make sense of the best insurance coverages for you as a Lyft driver, you’ll want to consider these tips.

Research the Company’s Policy Options

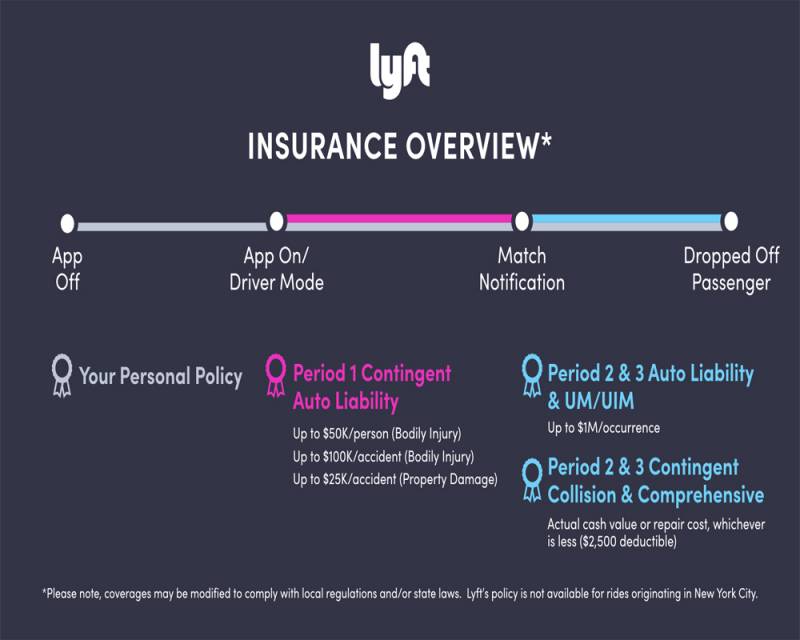

Before looking into your own personal auto insurance, you first should assess the commercial auto insurance that Lyft provides. Every driver has access to the same four types: contingent comprehension and collision, contingent liability, and uninsured/underinsured motorist.

When you’re driving and haven’t picked up a user, the contingent liability coverage kicks in. Under this policy, there is no deductible. You can, however, adjust the coverage to meet with state regulations. As soon as you pick up a Lyft user, the primary liability coverage is enacted. It lasts all the way until the Lyft user arrives at their destination. The policy covers up to $1 million in damage per accident.

The collision and comprehensive coverages still apply regardless of whether you’re at fault for the damage or not. You’ll pay a deductible and both take care of physical damage. The comprehensive portion covers a lot of potential scenarios, including natural disasters, fire, and even vandalism.

Lastly, there is uninsured/underinsured motorist protection. It’s designed to cover medical costs or damage that resulted from a driver that doesn’t have insurance or enough insurance. Up to $1 million in damage protection is provided per accident.

Buy Your Own Commercial Insurance

In most cases, Lyft will let you buy your own commercial insurance if you want additional protection or prefer to choose your own policy. If you’re afforded this option, there are some tips you need to keep in mind so that you get the best policy at the best rate.

Whatever insurance you decide to go with, you should strongly consider increasing your deductible. This is the amount of money you pay out of pocket before the auto insurance policy kicks in. The higher your deductible is, the lower your premiums – monthly payments – will be. After a while, the extra costs you pay on your deductibles will be off-set by the premium savings. It’s absolutely critical, though, that you find a deductible that you can truly afford.

You should also know what your commercial auto insurance covers. Today, it typically covers auto liability coverage, medical payment coverage, physical damage and collision coverage, and uninsured motorist protection.

Auto liability coverage is extremely useful when you cause the accident. Even if you’re the perfect driver, accidents are sometimes unavoidable. At least when you have this form of protection, you won’t have to worry about the repair costs to the other person’s vehicle. You also won’t be responsible for any legal expenses that occur because of the other driving suing you for their medical expenses.

For injuries that are severe, going to the hospital and receiving medical treatment may be required. These bills are not cheap, especially if your injuries require complex surgeries. That’s why it’s important to look for commercial auto insurance that provides medical payment coverage. It takes care of your medical costs, as well as the medical expenses that occupants in the vehicle experience. You’ll receive this coverage no matter who caused the accident.

Physical damage coverage, as mentioned earlier, takes care of damage that results because of theft, vandalism, and unforeseen weather elements. You never know what will happen on the road as a Lyft driver, but this additional coverage helps you drive with a peace of mind.

Whatever type of commercial coverage you get, just make sure it’s absolutely needed. There may be instances when choosing just a few types, or just one, is best to help lower your monthly costs.

Select the Right Personal Coverage

There will be times when you don’t have a Lyft user in your vehicle. In this instance, your personal auto insurance is what remains active. So that you’ll be ready for whatever adverse road scenario comes your way, it’s paramount to select the right personal coverage.

Like commercial auto insurance, there are several different types. You should start by seeing what your state requirements are. These can vary from state to state – so you’ll want to do your research to abide by the laws. Some states, for example, will require you to carry personal injury protection while others do not. Then there are states that require uninsured motorist protection as a precaution. Once you find out what’s required and what’s not, you can start deciding on the additional coverage you need.

As far as personal coverage, there are many levels of coverage you can get. These include:

- Liability

- Uninsured and underinsured motorist protection

- Comprehensive coverage

- Personal injury protection

- Collision coverage

- Medical payments coverage

Which protection you ultimately choose while driving for Lyft depends on your driving habits and particular financial situation. You can also narrow down your choices by assessing common threats that you’ll probably experience while working for this company.

After assessing the coverage types, it’s time to think about payment options. Different insurance companies offer different plans. Some companies require you to pay money up front, while others offer payment plans. The latter is beneficial if you don’t have a lot of money on hand. The up-front payment plans are ideal if you don’t want to think about your insurance costs later on down the road.

Finally, you should compare different quotes in order to find the most competitive rate. Searching online is probably the most convenient way to do this, as it saves you time and energy. You’ll be required to enter some personal information, including name, contact info, driving records, and vehicle data.

Consider Rideshare Insurance Options

The last, and perhaps most important, type of insurance you’ll want to consider while driving for Lyft is known as rideshare. It covers any damages that occur within a certain window: when the app is active and you’re waiting to get a customer.

You’ll need this type of coverage for many reasons. For one, a lot of personal insurance companies will not grant coverage once they find out that you’re using your vehicle for commercial transportation. They see it as an added liability, and this can result in decreased coverage or them dropping your coverage completely. In either case, rideshare insurance gives you much-needed protection for the foreseeable future or until you find another personal insurance auto claim.

If you’re dropped by an insurance provider, chances are your rates will only increase from this point on. You don’t have to worry about increased rates when you have rideshare coverage, however.

Like commercial and personal auto insurance, there are many different types of rideshare policies you can select from. One of the most common is a policy that only covers you through period one – which is the time you’re online and don’t have any customer requests yet. Cutting out the other periods saves you some money, and you may not need them anyway if you have additional insurance from Lyft or by your own means.

Duplicate coverage is also available, which covers you during periods 2 and 3. This option gives you added confidence because whether you’re on your way to pick up a customer or they’re already in your vehicle, coverage is provided. Then there are personal rideshare policies you can get, which won’t get cancelled if the insurance company finds out that you use your vehicle for commercial transportation.

Whatever type of policy you get, there are money-saving measures that you shouldn’t overlook. This starts with the vehicle you drive. If you plan on driving for Lyft full-time, you obviously want to choose a vehicle that has generous safety ratings. Look for vehicles with innovative safety features, such as anti-locking disc brakes, lane-departure warning, forward-collision control, and rear-view cameras. These added safety features help you avoid costly accidents – which rideshare insurance providers take note of.

You also should keep a clean driving record. The less accidents there are on your record, the less your rideshare insurance coverage will cost. There are plenty of ways you can keep a clean driving record. Always observe traffic signs and keep a manageable speed at all times. Lastly, you can save money on rideshare insurance by shopping around. Compare different quotes online and see which company offers a policy that fits your particular budget.

As you can see, there are so many insurance options you can choose from when it comes to driving for Lyft. Assess each option and think about what coverage you’ll need the most long-term. Only then can you drive with a peace of mind, knowing whatever accidents come your way will be taken care of financially.

Sources:

5 Safety Features That Can Save You Money on Car Insurance, nerdwallet.com (https://www.nerdwallet.com/blog/insurance/safety-features-car-insurance/)

{kind=link}

{kind=link}