Let's face it: college is an incredibly expensive life stage.

For most of us, it's also a life stage where money is tight. Therefore, it's no surprise that 70% of college students feel stressed about their finances, according to a study conducted at Ohio State.

Thankfully, there are a variety of freebies for students that can help cut down on monthly expenses to make college life more manageable.

Want some other quick money wins? Checkout:

- Scrambly: Get paid to play fun mobile games and for downloading cool apps!

- Branded Surveys: Share your opinion to get gift cards and free cash!

Free Stuff For Students You Can Claim Right Now

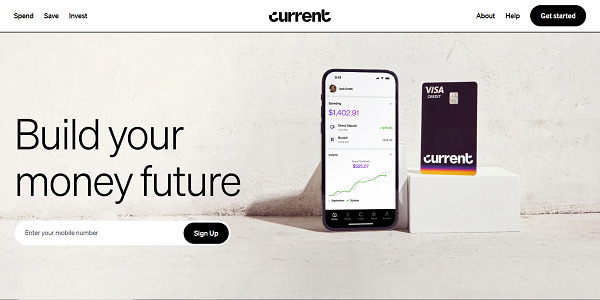

1. No-Fee Bank Accounts

If you pay monthly banking fees as a student, you need to make a change ASAP.

Almost every major bank has some sort of student bank account that carries zero monthly fees. Plus, many of these accounts have low minimum balance requirements, overdraft protection, and even have sign up bonuses if you're lucky.

Current is the perfect example. It has a nice $50 sign up bonus and doesn't charge monthly fees. Plus, it pays out 4% APY on up to $6,000 and can even help you build your credit!

This is a great way to earn passive income on some extra savings. And I like that Current is student-friendly and can help you gradually build up your credit.

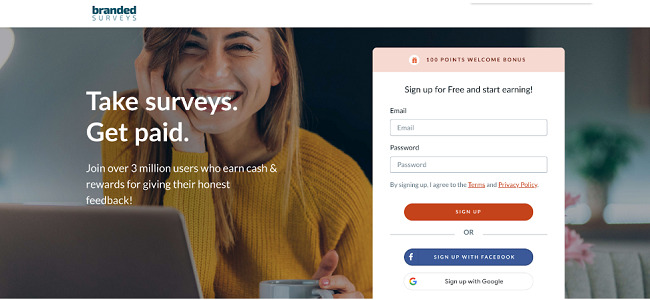

2. Free Gift Cards

How does a steady stream of free gift cards in your pocket sound?

I know this helped me out a ton as a student. And the great news is that you can enjoy the exact same thing if you know the right reward websites and apps to use. Some of my favorite options include:

All of these websites let you earn gift cards and cash just by sharing your opinion or by completing easy online tasks. And this is the perfect side hustle you can do between your classes when you're not studying.

Get started with Branded Surveys!

3. A Free You Need A Budget (YNAB) Membership

If you struggle with tracking your finances, scoring a free YNAB Membership is a great way to get back on track.

YNAB is a popular budgeting app for Android and iOS that makes it easy to track your spending. Through the app or website interface, users can setup goal tracking, budget categories, and gain a better understanding of where their money is going each month.

YNAB normally costs $99 per year. But right now, you can get a full year for free if you're in college. All you have to do to unlock this software is to email YNAB with proof that you are a student and you're off to the races!

You can also check out other leading budgeting apps, like Rocket Money, for even more options to save more money each month!

Get your budget on track with YNAB today!

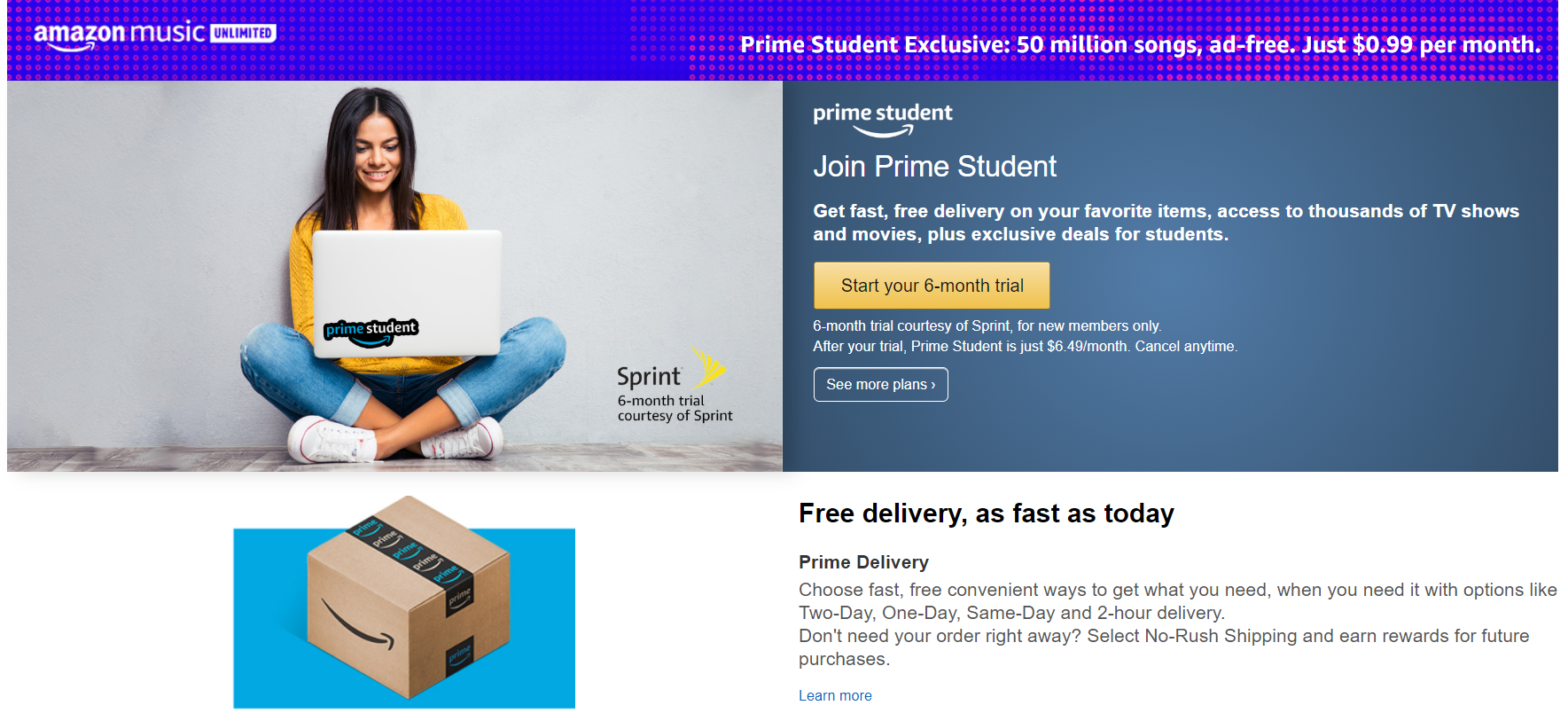

4. Free Amazon Student

Amazon Student is hands down one of the most comprehensive way to find freebies for college students. I didn't use this during my time in college, and just signed up for free Amazon Prime. However, Amazon Student is way more robust.

Some of the main perks offered by Amazon Student include:

- Free Prime delivery

- Exclusive travel deals

- Huge discounts on Amazon video, music, and kindle

- Free food delivery from Grubhub

- Discounts to products like Course Hero and Calm

The free trial is only 6 months, so be sure to activate this during a time you can maximize savings and freebies! If you continue your membership, you still save 50% on Prime since you're a student.

These 10+ Companies Give Free Stuff To People.

5. Free Grocery Discounts

If you live in a “student-town,” many grocery stores probably have student discount days that offer 5-10% off your grocery bill.

Shopping on specific student deal days is such an easy way to save money. While this isn't exactly the purest way to get free stuff as a student, it's still an easy way to cut down on your bills.

I did this all the time in my college town. On Tuesdays, students got 10% off at most grocery stores, so this was an easy win.

Extra Reading – How To Get Free Starbucks.

6. Discounted Music & Free TV Streaming

Any student understands how important music is. From late-night study binges to being able to confidently secure the aux cable, having easy and affordable access to music is critical.

Thankfully, top music streaming services like Spotify and Apple Music both offer some decent discounts on their services, as well as some streaming freebies for students.

Here are the specific student deals:

- Spotify Student Premium – Spotify Premium, ad-supported Hulu, and Showtime for $5.99/month. This is nearly $22/month in savings.

- Apple Music Student Subscription – Discounted Apple Music for 48 months ($4.99 per month) plus free Apple TV+.

Signing up for a student discount just requires proof that you are a student or a student email address, so this is an incredibly easy way to save and get some free streaming services.

7. Free Resume & Editing Services

Almost every college or university will have resources in place to help students with their resume or essay editing. Usually, these services are located in the library or career service building, but they are seriously underutilized.

If you pay a professional to edit your resume or essay, you're looking at a pretty hefty bill. Next time you need help with career guidance or improving your grades, be sure to poke your head around campus or to check your college's website.

Chances are, there's a way to find free help from trained professionals or, at the very least, other students with some training.

The Best Places Giving Free Things On Your Birthday.

8. Reward Apps

While this isn't exclusive to students, the world of reward apps is another awesome way to save money and also earn some freebies.

When you're in school, it can be difficult to qualify for a lucrative cash back credit card. Alternatively, you might prefer sticking with a debit card. In either case, you can at least get in on some cashback action with a few nifty apps and shopping extensions like:

-

- Capital One Shopping. Automatically apply available coupon codes at checkout at thousands of popular stores. Note, Capital One compensates us for using the provided link.

- Ibotta. A leading grocery rewards app.

- Upside. My favorite way to earn cash back when buying gas.

- Checkout 51. One of the best grocery and gas reward apps around, which can help you save on your monthly living expenses.

- Rakuten. My favorite cashback website. If you shop online, you absolutely need to use Rakuten first to score easy savings.

- Fetch Rewards. Another great grocery reward app that's ideal if you don't find success with Checkout 51.

When it comes to finding free things for students, sometimes it's best to keep things simple and to stick with what already works!

9. Scholarships & Grants

This is an obvious one, but it needs mentioning. After all, did you know that an estimated $100 million in scholarship money goes unclaimed every year?

If you're in high school or college, consider searching for some scholarships or grants you can apply to. Websites like Scholarship Portal are an excellent starting point for your search.

10. Free Software For Students

College classes sometimes require students to make additional software purchases. Plus, there are certain software suites out there that you sort of need to actually function in this day and age (I'm looking at you, Microsoft Office).

Before you purchase anything, check your college website for a free software section. I downloaded my entire Microsoft suite for free, plus some analytics software I needed for Psych classes. Plus, there are plenty of websites or corporate deals specifically designed to save students money.

Some of the best websites for finding free software as a student include:

- On The Hub – Up to 90% off many popular software suites.

- Tableau – Free data analytics software that is required for some classes.

- Adobe – 60% off the Adobe Creative Cloud.

- Autodesk – Free Autocad and other software that is crucial for engineering or science students.

- JetBrains – Useful for programming students since it's like GitHub.

- Free Microsoft Office – Probably one of the best college freebies that's out there.

If you want to take things to the next level, I also suggest checking out Reddit Freebies to find global and local signup bonuses or freebies every single day!

Extra Reading – How To Get Some Free PayPal Money.

11. LinkedIn Student & LinkedIn Learning

LinkedIn is a great platform for networking and finding job opportunities. However, LinkedIn also has some useful resources for students and an incredibly valuable LinkedIn Learning hub.

LinkedIn Learning offers tons of incredible courses to learn new skills like programming, Excel, business strategy, or pretty much any subject. The platform offers a one month free trial, although when I was a student, our school made it possible to signup for free.

I'm not sure if this is the case anymore, but keep an eye out for offers or make use of the free month.

12. Free Textbooks

Buying and reselling textbooks was one of my favorite college side hustles. However, like any other student, I absolutely despite textbooks and the companies that produce them.

Besides, spending money on textbooks is sometimes a complete waste. I mean, I'm sure you've purchased a textbook before after the professor recommended it, only to find it wasn't needed for the course.

Stop doing this. After all, one of the most valuable freebies for students that exists is the library. Almost every school has a textbook rental program that lets students check out books for a few hours at a time. Plus, if you can't find a required textbook in the rental section, you can usually pressure your professor into getting it supplied.

This single tip will save thousands over the course of a degree. Plus, you can also find free college textbooks on Reddit with a bit of know-how.

You can also checkout Abebooks for cheaper college textbooks! This is where I bought everything from when I was in school if I couldn't find it for free.

13. Free Condoms & Health Supplies

You'd be surprised at the sorts of free things that are offered by your campus' health clinic.

Free condoms are pretty much a given at any health center on campus. However, I know some schools provide free feminine products, or, at the very least, some free/discounted pharmacy products that you're sure to need during the year (like vitamins, cold medications, or Advil).

This won't save you a ton of money, but hey, you might as well make the most of your tuition money.

14. Free Events

I already mentioned that many museums offer free or heavily discounted admission for students. However, you should take some time to explore your own city or campus for more events.

College-sponsored events are a pretty great way to have fun without having to spend anything. Get some friends together to watch a sports game, or go to a trivia night on campus.

There's truly no excuse for being a hermit when you go to college, even if you are broke…the number of free events that go on is unbelievable (unless your school sucks).

15. Free Eye Exams, Dental Checkups, Haircuts, & Physiotherapy

Now, this category isn't exactly a student freebie since part of your tuition is dedicated to covering these sorts of services.

However, if you can't opt-out of paying for these services, you might as well make the most of them. Most schools cover a portion of health-related expenses up to a certain dollar value, and the quality isn't bad at all.

I opted-out of my dental plan, but I got regular eye exams on campus for free. Some of my friends took advantage of the physio program, and even if you aren't hurt, you can go for a massage to destress.

16. Free & Discounted Clothing For Students

You don't have to break the bank to dress well during school.

There are plenty of ways to get free or heavily discounted clothing as a student. Some campuses offer a donation bin or ‘take one, leave one' program which can be a great way to find new pieces or to exchange items of clothing.

Additionally, many stores offer student discounts or just have affordable clothing in general:

- Thrift stores – Do most of your shopping here if you're a student, trust me.

- Goodwill – Goodwill offers plenty of student discount days.

- Toms – Students save 10% with the code STUDENT10.

- Banana Republic – Students save 15%.

- UNiDAYS – Offers thousands of student discounts for various retailers, including many clothing brands.

There are probably other clothing stores with student discounts in your town as well, so keep an eye out for deals!

Extra Reading – How To Get Free Clothing.

Final Thoughts

As mentioned, it's things like budgeting, living within your means, and starting a side gig that will truly relieve financial stress during college. After all, finding different freebies for students isn't going to revolutionize your finances in college.

However, every little bit helps, and if you can easily save money just by being a student, you might as well make the most of it.

If there's one thing you take away from this list of free stuff for students, please let it be the student discount card at the very least.

This list contained plenty of great money saving options, but trust me, getting a student discount card will do some serious good for cutting down your monthly spending.

Want even more ideas to make and save money? Checkout: